Alexey Strygin on billionaire mortality, selection bias and what the funding gap reveals about aging research.

Imagine you’ve finally joined the ranks of the ultra-wealthy. The world’s best doctors are on call, your schedule is optimized, your diet calibrated, your biomarkers monitored. If money can buy anything, surely it can buy time. Or can it? With access to elite healthcare, personal trainers and experimental therapies, one might expect billionaires to meaningfully outlive the rest of us. The question is simple: do they?

To explore this, I examined deaths among billionaires between 2015 and 2025, compiling 389 cases representing approximately $2.2 trillion in wealth at the time of death. Over that decade we lost industrial architects, fashion magnates, technology pioneers and financial strategists – individuals who collectively shaped markets and industries across the globe.

What the data show

Three patterns emerge immediately: six helicopter crashes, a surprisingly large “cause not disclosed” category and, among known causes, a striking predominance of aging-related deaths. In roughly 90% of cases where cause was available, death followed the familiar arc of late-life disease or quiet physiological decline. Billionaires, it turns out, die much like everyone else – gradually losing physical and cognitive capacity before succumbing to cardiovascular disease, cancer or other age-associated conditions.

External causes account for about 7% of deaths where cause is known, slightly above the 2.5–6% range typical of high life expectancy countries. However, this likely reflects reporting bias; dramatic events such as aviation accidents or homicides generate headlines, while a conventional death from heart failure often goes unreported in detail. When calculated against all deaths, including those without disclosed causes, external causes fall to roughly 5%.

Six helicopter crashes in a decade, in a population numbering only a few hundred, is nevertheless notable. Helicopters are frequently used to save time; in these instances, they shortened life instead. The most prominent example in the dataset is Petr Kellner, whose aircraft crashed during a heliskiing trip in Alaska.

A further observation concerns opacity. For approximately 30% of cases, I was unable to identify a documented cause of death in public sources. Notably, the average age within this undisclosed group was higher than the overall sample, suggesting that aging-related causes may in fact be understated in the published figures.

Can wealth meaningfully extend life?

The central question remains: does extreme wealth translate into longer life?

As a benchmark, I compared billionaire ages at death with Hong Kong, which consistently ranks among the world leaders in life expectancy and offers a useful proxy for what top-tier public health systems can achieve.

Among women, the findings are counterintuitive. Female billionaires in the dataset had a mean age at death of 83.5 – approximately 4.5 years below Hong Kong’s female life expectancy at birth of 88.0. While this is a crude comparison and requires refinement, it places female billionaire longevity closer to several Eastern European nations than to the global frontier.

Perhaps more striking, the typical female survival advantage nearly disappears. Male billionaires died at a mean age of 82.8; females at 83.5 – a difference that is not statistically significant. With only 32 female deaths in the dataset, caution is warranted, yet the pattern is difficult to ignore.

At first glance, male billionaires appear only marginally advantaged. Their mean age at death roughly matches Hong Kong’s male life expectancy at birth and falls below life expectancy at age 50. However, such comparisons are imperfect because billionaire status is not assigned at birth; it is attained later in life.

To obtain a more meaningful estimate, I conducted a person-years analysis, comparing observed billionaire deaths across age bands to expected deaths based on Hong Kong mortality tables. This approach suggests that male billionaires experience approximately 29% lower mortality than the general population benchmark, with those reaching 50 living to a median age of 90 – around four years beyond comparable peers.

This figure should be interpreted as an upper bound. Several selection effects likely inflate the apparent advantage: survival to wealth accumulation, personality traits conducive to both business success and health maintenance and the possibility that deteriorating health may lead individuals to fall below billionaire thresholds before death, thereby exiting the dataset.

The ceiling at 90

Even if we accept the upper-bound estimate of a 29% mortality advantage, the benefit is not evenly distributed across the lifespan. The advantage appears concentrated between ages 60 and 89, where billionaire mortality rates are materially lower than the Hong Kong benchmark. In those decades, access to high-quality healthcare, preventative screening and early intervention likely matters.

After 90, however, the advantage effectively disappears. Mortality rates among billionaires in their nineties become statistically indistinguishable from the general population in one of the world’s longest-lived societies. At that point, the Gompertz curve asserts itself. Whatever protection wealth confers in earlier decades no longer appears sufficient to bend the underlying biology.

This is the key constraint. Extreme wealth may defer risk; it does not abolish it.

What the numbers suggest

The overall pattern is sobering.

For men, the longevity dividend associated with billionaire status likely falls somewhere between zero and four additional years relative to the healthiest national population. Selection bias complicates precision, but the magnitude is clearly incremental rather than transformative.

For women, the picture is more ambiguous. Female billionaires in the sample died, on average, several years earlier than the Hong Kong female benchmark. The traditional five-to-seven-year female advantage over men narrows almost to zero in this group. With limited sample size, caution is essential, yet the signal is noteworthy.

For those who reach 90, wealth confers no detectable survival edge. Mortality rates converge. No financial portfolio has yet negotiated an exemption from exponential aging dynamics.

The most advanced healthcare available today appears capable of managing age-related disease – cardiovascular events, malignancies, metabolic dysfunction. It does not meaningfully alter the rate at which biological aging progresses. After a certain point, spending more on personal optimization yields diminishing returns.

That conclusion should not be read as fatalism. It points instead to where leverage truly lies.

Implications for today’s ultra-wealthy

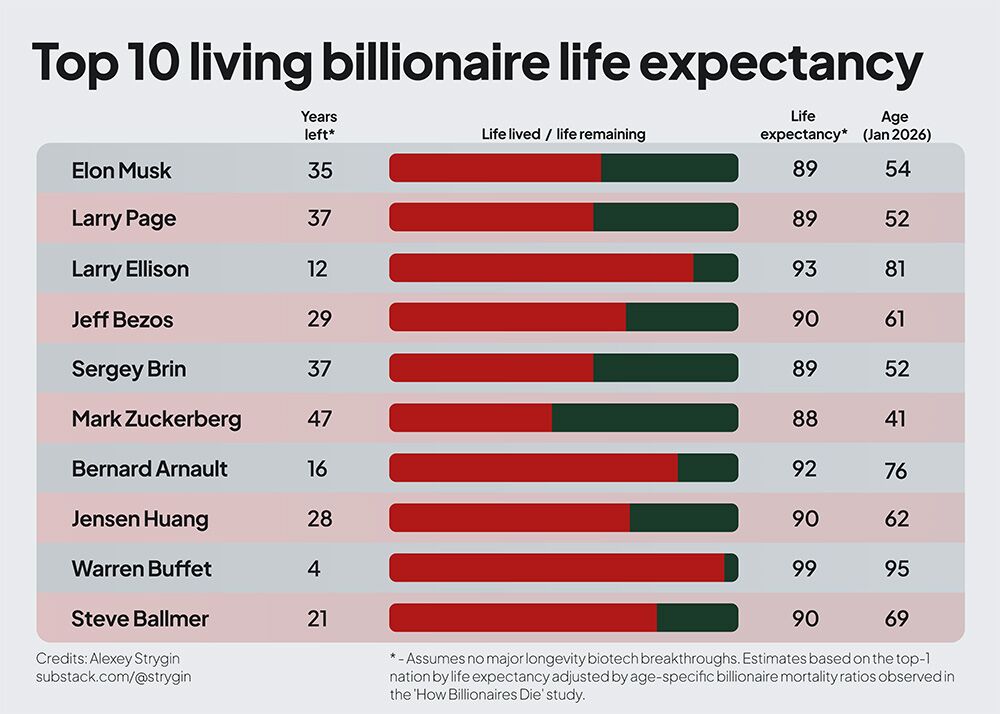

To ground this analysis, I modelled projected life expectancy for today’s ten richest individuals, applying the observed mortality ratios to Hong Kong life tables. Nine of the ten have already passed the midpoint of their expected lifespan under these assumptions.

The message is not that wealth is irrelevant. It clearly correlates with lower mortality across key decades of late adulthood. The message is that its effect size is bounded.

Health optimization – executive diagnostics, concierge medicine, preventative interventions – may detect and manage disease earlier. It cannot, on present evidence, fundamentally slow the biological processes that drive aging itself.

The constraint is structural, not behavioral.

Where the leverage truly sits

If personal expenditure on healthcare has a ceiling, research investment may not.

Historically, durable gains in life expectancy have come from technological progress: sanitation systems, antibiotics, vaccines. Each extended life by addressing systemic drivers of mortality. Today, most deaths in high-income countries are aging-related. Extending life meaningfully from here likely requires addressing aging biology directly.

The disparity between resources lost to aging and resources committed to solving it is striking. Over the past decade, 246 billionaires with a combined net worth of approximately $1.56 trillion died from aging-related causes. Over roughly twenty-five years, estimates suggest that ultra-wealthy individuals have collectively directed around $5 billion toward longevity ventures – approximately $200 million per year. The average billionaire dying of aging in this dataset held more wealth individually than the entire class has allocated to longevity research over a quarter century.

The asymmetry is difficult to ignore.

Capital allocation across scales

The practical question becomes one of deployment.

At any level of wealth, advocacy and awareness can shift policy priorities. The expansion of federal dementia funding in the United States over the past decade illustrates how sustained focus can redirect billions toward research. Practical first steps for advocacy include supporting organizations like Vitalism, the Longevity Biotech Fellowship, or The Longevity Initiative.

At tens of millions, philanthropic and venture capital can support proof-of-concept aging trials that neither traditional pharma nor government agencies readily fund. Regulatory engagement with aging as an indication is emerging, but early-stage translational work often depends on risk-tolerant capital.

At hundreds of millions, the opportunity expands to institution-building and longitudinal biobanks – infrastructures that generate durable scientific returns. The UK Biobank, built at a cost measured in hundreds of millions, has contributed to tens of thousands of publications and numerous therapeutic developments. A biobank designed explicitly around longitudinal aging phenotypes could accelerate the field materially.

At the billion-dollar scale, precedent exists for coordinated scientific megaprojects. The Human Genome Project required several billion dollars and catalyzed entire industries. Large-scale physics and space initiatives demonstrate that sustained capital, when directed at a singular aim, can reshape technological frontiers. An analogous effort targeting the mechanisms of aging would not be conceptually unprecedented – only ambitious.

The central claim is straightforward: if the objective is to move the upper bound of human lifespan rather than marginally extend the median, the locus of action shifts from personal healthcare consumption to collective research investment.

A boundary revealed

The data from billionaire mortality do not show that money is powerless. They show that its power is constrained. Wealth appears to buy time primarily within the existing medical paradigm – earlier detection, better management, marginal delay.

Beyond that, biology reasserts control.

If there is a lesson here for the world’s richest individuals, it is not that health optimization is futile. It is that the most durable return on capital may lie upstream – in accelerating the scientific progress capable of altering the Gompertz trajectory itself.

Until then, even the largest fortunes remain subject to the same curve as everyone else.

Full methodology is posted here.

Special thanks to those who helped shape this research: Nathan Cheng, Alexander Fedintsev, Andrew Steele, Alex Sviridov, Kirill Denisov, Judith Mueller, Danila Immortalist, Yan Granat, Daniel Kravtsov, Adam Gries, Artemy Shumskiy, Mark Hamalainen, Vladimir Shakirov, Martin Borch Jensen, Rakhan Aimbetov, Mike Batin, Thomas Ahlström, Laurence Ion, Simon Steshin, Aaron King

About Alexey Strygin

Alexey Strygin is a bioentrepreneur focused on advancing longevity biotechnology. He is co-organizer of the Hackaging.ai Hackathon, Founder of Longevity Economics Institute and a Core Team Member of Viva.city.

You can check out or subscribe to his Substack HERE.